Best Bank Account Type for NRIs

Breaking down NRE, NRO, and FCNR accounts for NRIs.

When it comes to choosing the right bank account as an NRI, the options can feel overwhelming. Should you go with an NRE or NRO account for your savings? Or, if you’re considering fixed deposits, is NRE, NRO, or FCNR the better choice? Each account type has distinct features suitable for different needs, making the decision a critical one for managing your finances effectively.

In this newsletter, we break it all down for you. First, we’ll help you understand the basics of each account—NRE, NRO, and FCNR—and what they mean for you. Then, we’ll provide a clear comparison to guide your decision-making.

But First,

Can NRIs Hold Resident Savings Account?

You may be surprised to learn that you cannot continue with your savings or current bank account in India. As per Foreign Exchange Management Act (FEMA) guidelines, you must close your existing savings or current account or change the status to an NRO account.

What is an NRO Account?

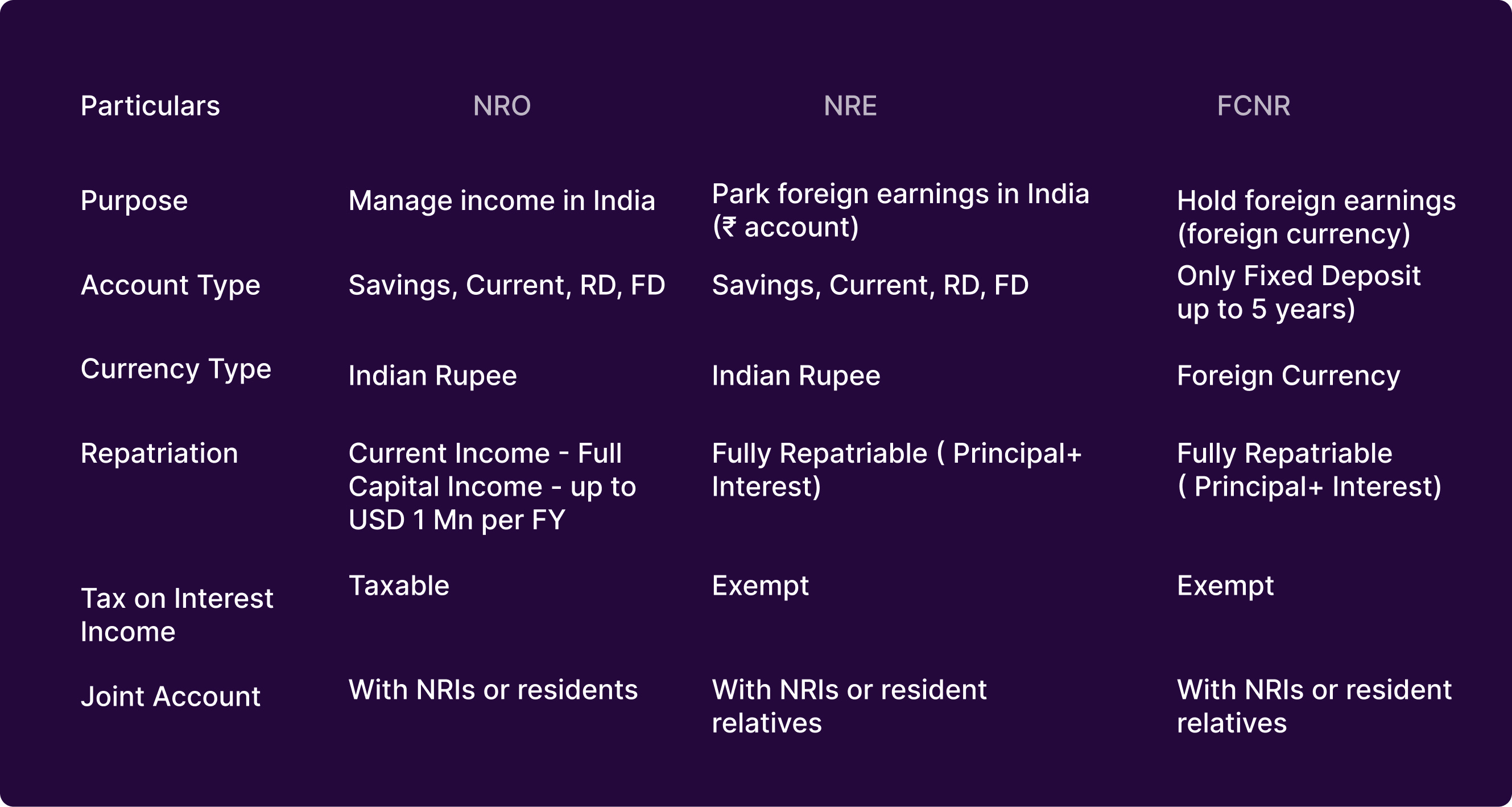

An Non-Resident Ordinary (NRO) bank account is a rupee-denominated bank account. It is ideal for managing earnings, local expenses, and investments from India, such as dividends, pensions, rent, and proceeds from the sale of immovable property.

Features of an NRO Account

Eligibility: NRIs/PIOs/OCIs can open; persons of Pakistan and Bangladesh origin require prior RBI approval.

Interest Rate: Varies by bank and account type.

Credits Allowed: Inward remittances, income earned in India, transfers from other NRO/NRE/FCNR (B) accounts, and rupee gifts/loans within prescribed limits under the Liberalised Remittance Scheme.

Debits Allowed: Local payments, transfers to other NRO accounts, and remittance of current income abroad without limit.

Tax Implication: TDS at 30% (plus surcharge and cess) on interest earned. Lower rates may apply under DTAA.

Please note that there is no upper limit on the amount of money that can be deposited in your NRO accounts.

What is an NRE Account?

Non-Resident External (NRE) account allows you to deposit your foreign currency earnings at prevailing exchange rates into a rupee-denominated bank account. The primary use of this account is to be able to deposit your foreign income and use it in India for transactions, payments and investments that need to be made in INR.

Features of an NRE Account

Eligibility: NRIs/PIOs/OCIs can open.

Interest Rate: Varies by bank and account type.

Credits Allowed: Inward remittances, interest, and investment proceeds; Transfers from NRE/FCNR accounts; Current income (rent, dividends, pension, interest)

(Note: Only repatriable credits are allowed.)

Debits Allowed: Permissible debits are local disbursements, remittances outside India, transfers to other NRE/ FCNR(B) accounts and investments in India.

Taxation: No tax since deposits are not earned in India

What is an FCNR Account?

Foreign Currency Non-Resident (FCNR) is a fixed-term deposit account that allows you to hold foreign earnings in foreign currency and earn interest in India. The FCNR account allows deposits for up to five years, maintained in foreign currencies like Pound Sterling, US Dollar, Japanese Yen and Euro, Canadian dollars, and Australian dollars. There is no exchange rate fluctuation as the deposits are in foreign currency.

Features of an FCNR Accounts

Eligibility: Available to NRIs, PIOs, and OCIs.

Interest Rates: Are competitive and depend on your tenure.

Credits Allowed: Inward remittance from outside India; interest accruing on the account; interest on investment; transfer from other NRE/ FCNR(B) accounts; maturity proceeds of investments (if such investments were made from this account or through inward remittance).

Debits Allowed: Local disbursements, remittances outside India, transfers to other NRE/ FCNR(B) accounts, and investments in India are permissible debits.

Taxation: Interest earned is tax-free in India.

NRO Vs NRE Vs FCNR Account

Which account is suitable for NRIs?

Choosing between NRO, NRE, and FCNR accounts depends on your financial goals and income sources:

An NRO Account is suitable for managing income earned in India, such as rent, pension, or dividends.

An NRE Account is ideal if your primary income is from abroad and you wish to use that money in India. Either for investments or expenses. It offers tax-free interest and unrestricted repatriation of funds.

The FCNR Account is a fixed deposit account. It helps safeguard foreign earnings in a foreign currency, protect against exchange rate risks, and earn tax-free interest in India.

You can select the account type based on where your earnings originate and how you wish to use the funds in India.

Open an NRE/NRO Account with iNRI

At iNRI, we make it easy to open an NRE/ NRO account with top Indian banks in India —hassle-free and from the comfort of your home.

No stress, no paperwork delays—just a seamless process to help you manage your finances effortlessly.